SIP vs. Lump Sum Investments: Which is Better for Indian Investors?

Feb 6, 2025

In India, where financial goals range from buying a home to securing a child’s education, investing wisely is non-negotiable. We have been asked this question many times: “Which is better? Systematic Investment Plans (SIPs) or Lump Sum investments? Should I invest ₹10,000 monthly via SIP or deploy ₹1.2 lakh as a one-time lumpsum?” The answer depends on your financial situation, risk appetite, and market dynamics. Let’s decode both strategies to help you make an informed choice.

Understanding SIPs: The Power of Discipline

SIPs allow you to invest a fixed amount (as low as ₹500) in mutual funds at regular intervals (monthly/quarterly). This approach is akin to a recurring deposit but with market-linked returns. Popularized by Indian mutual fund houses, SIPs have become synonymous with disciplined investing.

How SIPs Work

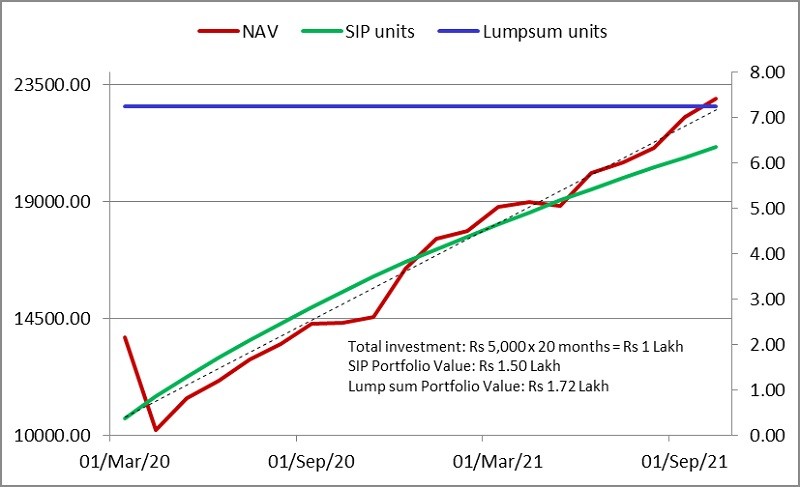

Imagine investing ₹5,000 monthly in an equity fund. If the NAV (Net Asset Value) is ₹100 in January, you get 50 units. If it drops to ₹80 in February, you get 62.5 units. Over time, this rupee cost averaging lowers your average cost per unit, insulating you from market volatility.

Pros of SIPs

Rupee Cost Averaging: Buy more units when markets dip and fewer when they rise, reducing average cost.

Low Entry Barrier: Start with as little as ₹500/month, ideal for salaried individuals.

Discipline & Compounding: Regular investments foster discipline, while long-term compounding grows wealth.

Emotional Resilience: Avoids the stress of timing the market.

Cons of SIPs

Lower Returns in Bull Markets: Gradual investment means missing out on full gains during rapid market rises.

Longer Horizon: Requires patience to build a sizable corpus.

Example: A ₹10,000/month SIP in Nippon India Growth Fund (2018–2023) would have grown to ~₹9.5 lakhs (15% annualized returns), despite 2020’s COVID crash.

Lump Sum Investments: Go Big or Go Home?

A lump sum investment involves deploying a large amount (e.g., ₹5 lakh) in one go. It’s suitable for those with surplus cash, like Diwali bonuses, inheritance, or sale of assets.

How Lump Sum Works

If you invest ₹2 lakh in a fund at an NAV of ₹50 during a market low (like March 2020), a 20% annual return would grow it to ~₹4.15 lakh in 4 years. But if the market crashes post-investment, recovery could take time.

Pros of Lump Sum Investments

Higher Potential Returns: Capitalize on market upswings immediately.

Simplicity: One-time decision, no monthly commitments.

Early Compounding: Entire sum starts growing from Day one.

Cons of Lump Sum Investments

Market Timing Risk: Poor timing can lead to short-term losses.

Emotional Challenges: Watching your ₹10 lakh dip to ₹7 lakh tests patience.

High Entry Barrier: Requires significant upfront capital.

Example: A ₹1 lakh lumpsum in Axis Bluechip Fund in March 2020 would have doubled by 2021. But the same investment in January 2020 would have dropped 30% during the COVID crash.

Key Factors to Decide Between SIP and Lump Sum

Factor | SIP | Lumpsum |

|---|---|---|

Market Conditions | Better in volatile or bear markets to average costs. | Ideal when markets are undervalued (e.g., post-corrections). |

Investment Horizon | >5 years: harness volatility. | <3 years: or arbitrage funds (lower risk). |

Risk Tolerance | Risk-averse: emotional stress. | Can stomach volatility: higher rewards. |

Financial Goals | Long-term goals: funds. (e.g., retirement) | Short-term goals: instruments. (e.g., car purchase) |

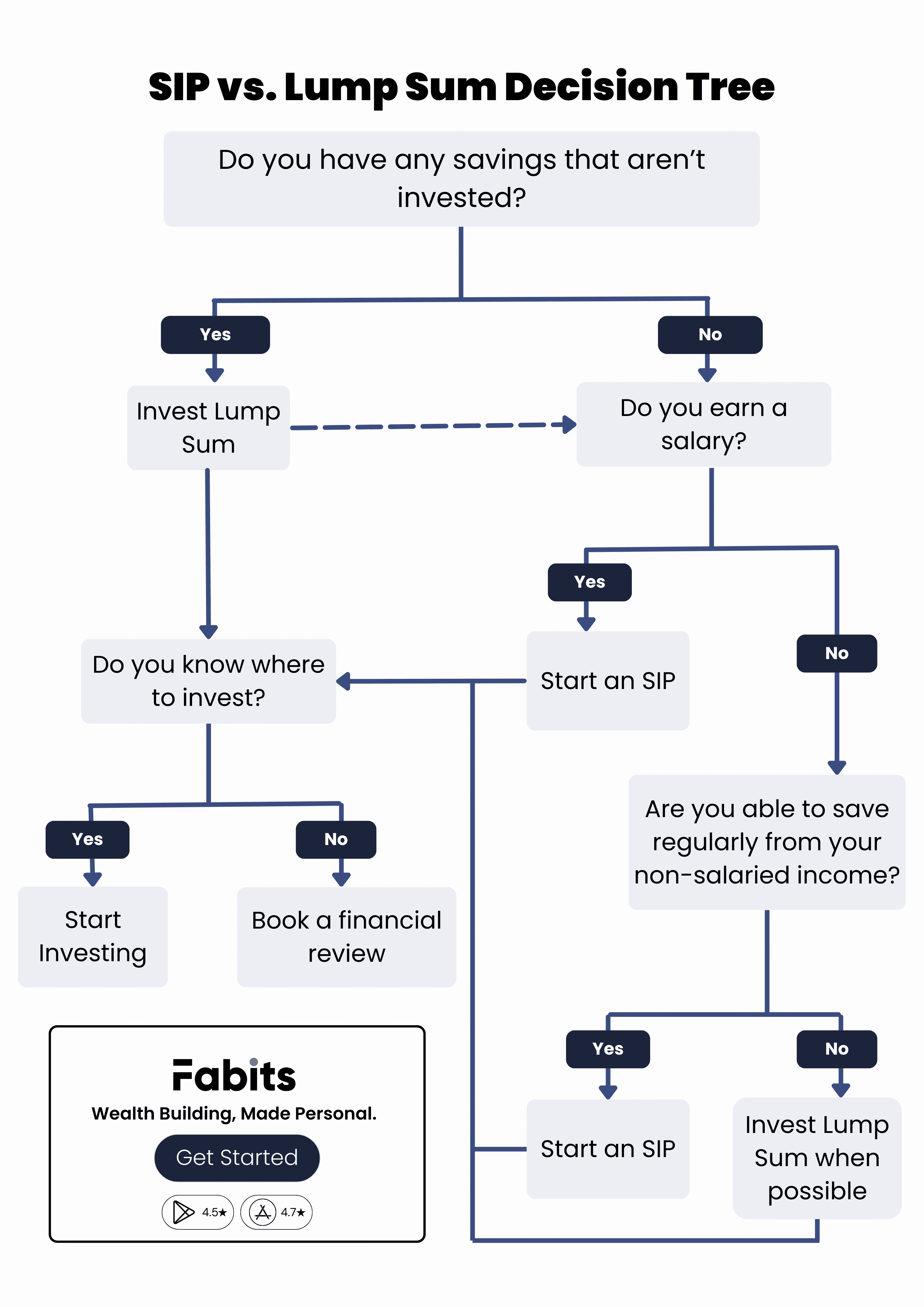

The Verdict: Mix and Match!

There’s no one-size-fits-all answer. Consider these scenarios:

Salaried Professionals: SIPs align with monthly cash flows.

Windfall Gains (e.g., inheritance): Allocate 60% lumpsum to equity and stagger the rest via SIPs.

Market Uncertainty: Use SIPs for 70% of your corpus and deploy 30% as lumpsum on dips.

Pro Tip: Use tools in Fabits to simulate SIP vs. lumpsum returns for specific funds.

Tax Implications of SIPs vs. Lump Sum Investments

Understanding the tax treatment of SIPs and lump sum investments is crucial for maximizing post-tax returns in India. For equity-oriented mutual funds, both strategies attract a long-term capital gains (LTCG) tax of 12.5% on profits exceeding ₹1.25 lakh if held for over 1 year. Short-term gains (held <1 year) are taxed at 20%. However, SIPs complicate this calculation slightly: each SIP installment is treated as a separate investment, meaning the holding period for each installment is tracked individually. For example, redeeming a 2-year SIP portfolio may have some units qualifying as long-term (older installments) and others as short-term (recent installments). In contrast, a lump sum investment has a single purchase date, simplifying tax calculations.

For debt funds, held for over 3 years, gains are taxed at 12.5% without indexation benefits (adjusting for inflation), regardless of SIP or lump sum. SIPs in ELSS funds (tax-saving mutual funds) offer Section 80C deductions up to ₹1.5 lakh annually, but each SIP installment has a 3-year lock-in period. While lump sum investments in ELSS lock the entire amount for 3 years, SIPs stagger the lock-in for each installment.

Always consult a tax advisor to optimize your strategy, as SIPs may require meticulous tracking of multiple tax lots, while lump sums offer simplicity but demand sharper market timing.

For most Indian investors, SIPs are a safer bet due to market volatility and disciplined wealth creation. However, lumpsum investments can shine during market corrections or for long-term horizons. Assess your risk appetite, financial goals, and market outlook before choosing. Better yet, blend both strategies! Consult a SEBI-registered advisor to tailor a plan for you.

Remember, whether SIP or lumpsum, starting early is the real game-changer. Kaal Kare So Aaj Kar, Aaj Kare So Ub!

In India, where financial goals range from buying a home to securing a child’s education, investing wisely is non-negotiable. We have been asked this question many times: “Which is better? Systematic Investment Plans (SIPs) or Lump Sum investments? Should I invest ₹10,000 monthly via SIP or deploy ₹1.2 lakh as a one-time lumpsum?” The answer depends on your financial situation, risk appetite, and market dynamics. Let’s decode both strategies to help you make an informed choice.

Understanding SIPs: The Power of Discipline

SIPs allow you to invest a fixed amount (as low as ₹500) in mutual funds at regular intervals (monthly/quarterly). This approach is akin to a recurring deposit but with market-linked returns. Popularized by Indian mutual fund houses, SIPs have become synonymous with disciplined investing.

How SIPs Work

Imagine investing ₹5,000 monthly in an equity fund. If the NAV (Net Asset Value) is ₹100 in January, you get 50 units. If it drops to ₹80 in February, you get 62.5 units. Over time, this rupee cost averaging lowers your average cost per unit, insulating you from market volatility.

Pros of SIPs

Rupee Cost Averaging: Buy more units when markets dip and fewer when they rise, reducing average cost.

Low Entry Barrier: Start with as little as ₹500/month, ideal for salaried individuals.

Discipline & Compounding: Regular investments foster discipline, while long-term compounding grows wealth.

Emotional Resilience: Avoids the stress of timing the market.

Cons of SIPs

Lower Returns in Bull Markets: Gradual investment means missing out on full gains during rapid market rises.

Longer Horizon: Requires patience to build a sizable corpus.

Example: A ₹10,000/month SIP in Nippon India Growth Fund (2018–2023) would have grown to ~₹9.5 lakhs (15% annualized returns), despite 2020’s COVID crash.

Lump Sum Investments: Go Big or Go Home?

A lump sum investment involves deploying a large amount (e.g., ₹5 lakh) in one go. It’s suitable for those with surplus cash, like Diwali bonuses, inheritance, or sale of assets.

How Lump Sum Works

If you invest ₹2 lakh in a fund at an NAV of ₹50 during a market low (like March 2020), a 20% annual return would grow it to ~₹4.15 lakh in 4 years. But if the market crashes post-investment, recovery could take time.

Pros of Lump Sum Investments

Higher Potential Returns: Capitalize on market upswings immediately.

Simplicity: One-time decision, no monthly commitments.

Early Compounding: Entire sum starts growing from Day one.

Cons of Lump Sum Investments

Market Timing Risk: Poor timing can lead to short-term losses.

Emotional Challenges: Watching your ₹10 lakh dip to ₹7 lakh tests patience.

High Entry Barrier: Requires significant upfront capital.

Example: A ₹1 lakh lumpsum in Axis Bluechip Fund in March 2020 would have doubled by 2021. But the same investment in January 2020 would have dropped 30% during the COVID crash.

Key Factors to Decide Between SIP and Lump Sum

Factor | SIP | Lumpsum |

|---|---|---|

Market Conditions | Better in volatile or bear markets to average costs. | Ideal when markets are undervalued (e.g., post-corrections). |

Investment Horizon | >5 years: harness volatility. | <3 years: or arbitrage funds (lower risk). |

Risk Tolerance | Risk-averse: emotional stress. | Can stomach volatility: higher rewards. |

Financial Goals | Long-term goals: funds. (e.g., retirement) | Short-term goals: instruments. (e.g., car purchase) |

The Verdict: Mix and Match!

There’s no one-size-fits-all answer. Consider these scenarios:

Salaried Professionals: SIPs align with monthly cash flows.

Windfall Gains (e.g., inheritance): Allocate 60% lumpsum to equity and stagger the rest via SIPs.

Market Uncertainty: Use SIPs for 70% of your corpus and deploy 30% as lumpsum on dips.

Pro Tip: Use tools in Fabits to simulate SIP vs. lumpsum returns for specific funds.

Tax Implications of SIPs vs. Lump Sum Investments

Understanding the tax treatment of SIPs and lump sum investments is crucial for maximizing post-tax returns in India. For equity-oriented mutual funds, both strategies attract a long-term capital gains (LTCG) tax of 12.5% on profits exceeding ₹1.25 lakh if held for over 1 year. Short-term gains (held <1 year) are taxed at 20%. However, SIPs complicate this calculation slightly: each SIP installment is treated as a separate investment, meaning the holding period for each installment is tracked individually. For example, redeeming a 2-year SIP portfolio may have some units qualifying as long-term (older installments) and others as short-term (recent installments). In contrast, a lump sum investment has a single purchase date, simplifying tax calculations.

For debt funds, held for over 3 years, gains are taxed at 12.5% without indexation benefits (adjusting for inflation), regardless of SIP or lump sum. SIPs in ELSS funds (tax-saving mutual funds) offer Section 80C deductions up to ₹1.5 lakh annually, but each SIP installment has a 3-year lock-in period. While lump sum investments in ELSS lock the entire amount for 3 years, SIPs stagger the lock-in for each installment.

Always consult a tax advisor to optimize your strategy, as SIPs may require meticulous tracking of multiple tax lots, while lump sums offer simplicity but demand sharper market timing.

For most Indian investors, SIPs are a safer bet due to market volatility and disciplined wealth creation. However, lumpsum investments can shine during market corrections or for long-term horizons. Assess your risk appetite, financial goals, and market outlook before choosing. Better yet, blend both strategies! Consult a SEBI-registered advisor to tailor a plan for you.

Remember, whether SIP or lumpsum, starting early is the real game-changer. Kaal Kare So Aaj Kar, Aaj Kare So Ub!

Get Started

Fabits (Shareway Securities Private Ltd.)

294/1, 1st Floor, 7th Cross Rd,

Domlur 1st Stage,

Bengaluru, Karnataka - 560071

SEBI Reg. No.: INZ000208134

AMFI Registration Number : ARN-310082

Segments: NSE CM - FO

CDSL Depository Participant: IN-DP-610-2021

GST NO: 29AALCS7597J1ZA

SHAREWAY SECURITIES PRIVATE LIMITED (FORMERLY KNOWN AS SHAREWAY SECURITIES LIMITED) Member of NSE – SEBI Registration number: INZ000208134, BSE Member ID: 61731 CDSL: Depository services through SHAREWAY SECURITIES PRIVATE LIMITED – SEBI Registration number: IN-DP-610-2021. Registered Address: old no 46 new no 6, Gilli flower, flat, 2nd floor, 23rd street, Anna Nagar East, Chennai 600102. Corporate Address: 294/1, 7th Cross, Domlur Layout above Union Bank, Bangalore - 560071. For any complaints pertaining to securities broking please write to rathi@fabits.com . Please ensure you carefully read the Risk Disclosure Document as prescribed by SEBI

Procedure to file a complaint on SEBI SCORES 2.0 (Android Application, IOS Application) : Register on SCORES portal. Mandatory details for filing complaints on SCORES: Name, PAN, Address, Mobile Number, E-mail ID. Benefits: Effective Communication, Speedy redressal of the grievances. Investments in securities market are subject to market risks; read all the related documents carefully before investing.

Attention investors:

1) Stock brokers can accept securities as margins from clients only by way of pledge in the depository system w.e.f September 01, 2020.

2) Update your e-mail and phone number with your stock broker / depository participant and receive OTP directly from depository on your e-mail and/or mobile number to create pledge.

3) Check your securities / MF / bonds in the consolidated account statement issued by NSDL/CDSL every month.

Attention Investors-

Prevent unauthorised transactions in your account. Update your mobile numbers/email IDs with your stock brokers. Receive information of your transactions directly from Exchange on your mobile/email at the end of the day. Issued in the interest of investors.

KYC is one time exercise while dealing in securities markets - once KYC is done through a SEBI registered intermediary (broker, DP, Mutual Fund etc.), you need not undergo the same process again when you approach another intermediary.

Dear Investor, if you are subscribing to an IPO, there is no need to issue a cheque. Please write the Bank account number and sign the IPO application form to authorize your bank to make payment in case of allotment. In case of non allotment the funds will remain in your bank account.

As a business we don't give stock tips, and have not authorized anyone to trade on behalf of others. If you find anyone claiming to be part of Fabits and offering such services, please call us.

Common Online Dispute Resolution Portal

© 2024, Shareway Securities Private Limited. All rights reserved.

Fabits (Shareway Securities Private Ltd.)

294/1, 1st Floor, 7th Cross Rd,

Domlur 1st Stage,

Bengaluru, Karnataka - 560071

SEBI Reg. No.: INZ000208134

AMFI Registration Number : ARN-310082

Segments: NSE CM - FO

CDSL Depository Participant: IN-DP-610-2021

GST NO: 29AALCS7597J1ZA

SHAREWAY SECURITIES PRIVATE LIMITED (FORMERLY KNOWN AS SHAREWAY SECURITIES LIMITED) Member of NSE – SEBI Registration number: INZ000208134, BSE Member ID: 61731 CDSL: Depository services through SHAREWAY SECURITIES PRIVATE LIMITED – SEBI Registration number: IN-DP-610-2021. Registered Address: old no 46 new no 6, Gilli flower, flat, 2nd floor, 23rd street, Anna Nagar East, Chennai 600102. Corporate Address: 294/1, 7th Cross, Domlur Layout above Union Bank, Bangalore - 560071. For any complaints pertaining to securities broking please write to rathi@fabits.com . Please ensure you carefully read the Risk Disclosure Document as prescribed by SEBI

Procedure to file a complaint on SEBI SCORES 2.0 (Android Application, IOS Application) : Register on SCORES portal. Mandatory details for filing complaints on SCORES: Name, PAN, Address, Mobile Number, E-mail ID. Benefits: Effective Communication, Speedy redressal of the grievances. Investments in securities market are subject to market risks; read all the related documents carefully before investing.

Attention investors:

1) Stock brokers can accept securities as margins from clients only by way of pledge in the depository system w.e.f September 01, 2020.

2) Update your e-mail and phone number with your stock broker / depository participant and receive OTP directly from depository on your e-mail and/or mobile number to create pledge.

3) Check your securities / MF / bonds in the consolidated account statement issued by NSDL/CDSL every month.

Attention Investors-

Prevent unauthorised transactions in your account. Update your mobile numbers/email IDs with your stock brokers. Receive information of your transactions directly from Exchange on your mobile/email at the end of the day. Issued in the interest of investors.

KYC is one time exercise while dealing in securities markets - once KYC is done through a SEBI registered intermediary (broker, DP, Mutual Fund etc.), you need not undergo the same process again when you approach another intermediary.

Dear Investor, if you are subscribing to an IPO, there is no need to issue a cheque. Please write the Bank account number and sign the IPO application form to authorize your bank to make payment in case of allotment. In case of non allotment the funds will remain in your bank account.

As a business we don't give stock tips, and have not authorized anyone to trade on behalf of others. If you find anyone claiming to be part of Fabits and offering such services, please call us.

Common Online Dispute Resolution Portal

© 2024, Shareway Securities Private Limited. All rights reserved.

Fabits (Shareway Securities Private Ltd.)

294/1, 1st Floor, 7th Cross Rd,

Domlur 1st Stage,

Bengaluru, Karnataka - 560071

SEBI Reg. No.: INZ000208134

AMFI Registration Number : ARN-310082

Segments: NSE CM - FO

CDSL Depository Participant: IN-DP-610-2021

GST NO: 29AALCS7597J1ZA

SHAREWAY SECURITIES PRIVATE LIMITED (FORMERLY KNOWN AS SHAREWAY SECURITIES LIMITED) Member of NSE – SEBI Registration number: INZ000208134, BSE Member ID: 61731 CDSL: Depository services through SHAREWAY SECURITIES PRIVATE LIMITED – SEBI Registration number: IN-DP-610-2021. Registered Address: old no 46 new no 6, Gilli flower, flat, 2nd floor, 23rd street, Anna Nagar East, Chennai 600102. Corporate Address: 294/1, 7th Cross, Domlur Layout above Union Bank, Bangalore - 560071. For any complaints pertaining to securities broking please write to rathi@fabits.com . Please ensure you carefully read the Risk Disclosure Document as prescribed by SEBI

Procedure to file a complaint on SEBI SCORES 2.0 (Android Application, IOS Application) : Register on SCORES portal. Mandatory details for filing complaints on SCORES: Name, PAN, Address, Mobile Number, E-mail ID. Benefits: Effective Communication, Speedy redressal of the grievances. Investments in securities market are subject to market risks; read all the related documents carefully before investing.

Attention investors:

1) Stock brokers can accept securities as margins from clients only by way of pledge in the depository system w.e.f September 01, 2020.

2) Update your e-mail and phone number with your stock broker / depository participant and receive OTP directly from depository on your e-mail and/or mobile number to create pledge.

3) Check your securities / MF / bonds in the consolidated account statement issued by NSDL/CDSL every month.

Attention Investors-

Prevent unauthorised transactions in your account. Update your mobile numbers/email IDs with your stock brokers. Receive information of your transactions directly from Exchange on your mobile/email at the end of the day. Issued in the interest of investors.

KYC is one time exercise while dealing in securities markets - once KYC is done through a SEBI registered intermediary (broker, DP, Mutual Fund etc.), you need not undergo the same process again when you approach another intermediary.

Dear Investor, if you are subscribing to an IPO, there is no need to issue a cheque. Please write the Bank account number and sign the IPO application form to authorize your bank to make payment in case of allotment. In case of non allotment the funds will remain in your bank account.

As a business we don't give stock tips, and have not authorized anyone to trade on behalf of others. If you find anyone claiming to be part of Fabits and offering such services, please call us.

Common Online Dispute Resolution Portal

© 2024, Shareway Securities Private Limited. All rights reserved.